Why Entry Method Determines Your Real Cost Basis for LTC Breakout Window

Litecoin is trading at $57.74 on March 17, 2026, pressing against the $57.78 resistance that analysts identify as a Fibonacci 61.8% retracement confluence and order block. The consolidation structure is tight: a $57–$59 range has contained price since early February, Bollinger Bands are compressing toward the midline, and ATR-based volatility is contracting. This is the pre-breakout setup that breakout traders watch for. It is also, for any trader who decides to buy Litecoin now, a setup where entry cost precision is unusually consequential.

The broader context emboldens the argument. The Fear & Greed Index sits at 16 (Extreme Fear) — a historically significant contrarian signal for assets with established market structure. The 2027 Litecoin halving cycle is approximately 16 months away, the historical accumulation window that has preceded LTC’s most sustained post-halving rallies. A live spot LTC ETF (LTCC) is now trading on Nasdaq. Two corporate treasuries have allocated a combined $173 million to LTC. LitVM, the EVM-compatible ZK-rollup that would bring smart contract and DeFi capability to Litecoin’s base layer, is in Q1 2026 testnet phase. The fundamental thesis for a medium-horizon position is not absent. What is often absent, for retail buyers entering via credit card or instant payment apps, is a clear calculation of what that entry actually costs — and how that cost interacts with the specific levels that define the current technical setup.

Why LTC and Why Now

The upcoming 2027 halving is the structural anchor for this narrative. Block rewards will be cut from 6.25 to 3.125 LTC, reducing the daily issuance rate in a market where demand from spot ETF flows and corporate treasury allocation has been building.

The near-term technical picture is nuanced. LTC is above EMA20 ($55.43), confirming a short-term bullish structure. However, the daily Supertrend remains bearish, and the 200-day SMA sits at approximately $83.76 — far above current price, representing the ceiling that any sustained rally must eventually clear. On-chain data shows large whale orders and buy dominance in both spot and futures markets, a positive structural signal. Counterbalancing that, the Age Consumed index is showing spikes in dormant wallet activity, which historically signals short-term local tops or redistribution by long-term holders.

The derivatives picture adds another layer. The long-to-short ratio reads 0.89 — bears are positioned in the majority. But the OI-weighted funding rate flipped positive on Sunday and currently stands at 0.0013%, meaning longs are paying shorts, which reflects a market where buyers are willing to pay a carry premium to maintain exposure. That is a cautious long bias, not a consensus directional call. The setup is a breakout preparation, not a confirmed trend: buying LTC here is a thesis-driven position, and the cost of entry is part of the thesis.

Cost Stack of Buying Litecoin Fast

When the decision to buy LTC is made, whether on a breakout confirmation or ahead of it, the purchase route determines a second, invisible price that never appears on the order screen. Credit card purchases, instant buy flows, and payment app on-ramps each add a cost layer that compounds the effective entry price.

The cost components that typically stack on a card-based or convenience-route LTC purchase:

- Platform or processing fee: 2–4%, charged explicitly or embedded in the quoted rate. The price shown on a card purchase screen is not the same as the LTC/USD spot rate.

- Spread: the gap between the quoted price and live spot, layered on top of the processing fee. On instant buy flows this is where most of the margin is captured invisibly.

- Cash advance classification: a material proportion of card issuers categorise crypto exchange transactions as cash advances rather than retail purchases. This triggers an upfront fee of 3–5% plus immediate interest accrual from settlement date, with no grace period. The buyer may not know which treatment applies until the statement arrives.

- Third-party processor markup: simplified swap services and some exchange convenience flows route through payment intermediaries that apply 0.5–1.5% on top of the exchange’s disclosed fee.

The all-in cost for a card purchase through a convenience flow commonly lands between 4% and 7%. A bank transfer or ACH route on the same platform typically costs 0.5–1.5% in exchange fees. The difference is the price of speed — and at current LTC levels, speed has a measurable interaction with the technical structure.

Break-Even Price for Current LTC Levels

With LTC at ~$57.74 and the immediate breakout resistance at $57.78 — a distance of $0.04 — the entry cost arithmetic is unusually precise. The $57.78 level is not an arbitrary round number; it is a volume-weighted order block and Fibonacci 61.8% retracement confluence that carries a 77/100 significance score in the current analysis. A decisive close above it targets $60.84 (5.3% upside) and $71.32 (23.5% upside) as the bull case. Rejection targets $56.94 first, then the $55.00 support base.

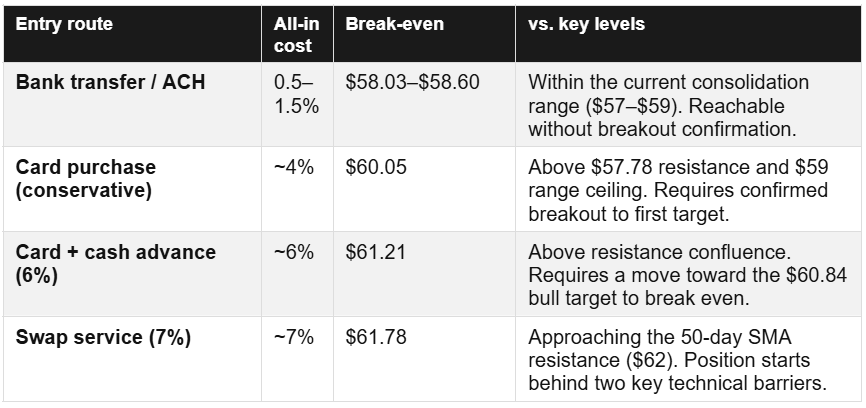

The table makes the interaction explicit: a bank transfer entry at $57.74 breaks even between $58.03 and $58.60, inside the existing consolidation range and achievable without any breakout. A credit card entry at the conservative 4% cost breaks even at $60.05 — above both the $57.78 resistance and the $59 range ceiling, requiring the breakout to have already delivered its first target before the position becomes profitable. At 6% all-in cost, break-even at $61.21 requires the rally to reach nearly the $60.84 bull target. At 7%, break-even sits at $61.78, approaching the 50-day SMA at $62 that represents the next significant overhead resistance.

The 14-day ATR is $2.07–$2.56. That is sufficient daily volatility to bridge the gap between a bank transfer and a card purchase break-even in a single session — but only if the breakout is real and volume-confirmed. The risk is that a 4–7% convenience premium converts a sound technical entry into a position that requires the entire bull case to simply reach parity.

On-Ramp Options and the LitVM Question

The purchase route decision is downstream of a more fundamental question: what is the intended use of the acquired LTC? The answer has structural implications for which on-ramp architecture is appropriate, and for how the withdrawal hold that accompanies most card purchases interacts with that intent.

Custodial exchange platforms, the most commonly used route for card purchases, typically impose a 24–72 hour withdrawal hold on credit card funded positions. The purchased LTC is available for on-platform trading immediately, but cannot be transferred to an external wallet until the hold clears. For a buyer whose plan is on-platform holding or trading, this is minor friction. For a buyer whose thesis involves the LitVM catalyst, the hold period is a measurable cost: if LitVM delivers EVM-compatible smart contract execution on Litecoin’s base layer, purchased LTC that cannot be moved on-chain is LTC that cannot participate in the earliest DeFi activity on that infrastructure.

Three on-ramp architectures cover the practical spectrum for a buyer deciding to buy LTC:

- Full custodial exchange: broadest asset access, order book depth, limit order capability. Card purchases subject to withdrawal holds. Appropriate when the plan is on-platform trading or holding with flexibility to move later.

- Direct-to-wallet swap services: buy Litecoin delivered to a user-specified wallet address on completion. No exchange custody; no withdrawal hold. All-in cost typically at the higher end of the card fee range. Appropriate when on-chain deployment or self-custody is the immediate objective.

- Payment apps and broker platforms: simplest UX, most restricted custody. LTC withdrawals are often unavailable entirely. Appropriate only for pure price exposure with no self-custody intent. Not appropriate if ecosystem participation or pre-halving accumulation in self-custody is the goal.

Bottom Line

The decision to buy Litecoin against a resistance confluence, with the halving 16 months out, ecosystem developments, and Extreme Fear sentiment providing a contrarian backdrop is a legitimate, multi-factor position thesis. No on-ramp route changes that thesis. What it does change is the effective cost basis from which that thesis begins, and the technical level that must be reached before the position moves into profit.

At a 4–6% card purchase premium, break-even requires the breakout to have already delivered its first target. At 0.5–1.5% via bank transfer, break-even is inside the existing consolidation range. The halving thesis and other catalysts are medium-horizon arguments that do not change the near-term arithmetic of entering at a premium above a breakout level that has not yet been confirmed.

0 Comments

Leave a comment